Summary

- Hedgewise has incurred losses of 5-10% since late January, depending on your product and risk level, but is only down slightly year-to-date and continues to outperform all major competitors.

- Much of the drawdown has been driven by simultaneous losses across all asset classes, which strongly suggests investor panic and confusion. Such scenarios have never lasted long historically and will likely soon reverse.

- Even if some of the worst-case scenarios come true, like stronger than expected inflation or a recession, both Hedgewise frameworks have held up well in such environments.

Stay Calm and Carry On: Putting Recent Losses in Perspective

Make no mistake: markets have been pretty wild for the past couple of weeks, and if it's started to make you nervous, you are human after all! It has been especially confusing because the swings are quite hard to explain: not all that much has changed in the economy since January, yet markets are suddenly terrified of inflation, government debt, volatility, and valuations. If you can't explain why people are selling now, it's also hard to predict when they will stop.

Since every investor on the planet has this same logic and fear, it's easy to see how it can all quickly turn into a frenzy. And yet, this story also justifies why short-term market volatility shouldn't worry you much at all. If people are panicking for no good reason, you can be almost certain that they are selling assets too cheaply, and that's really the worst possible time to change your approach.

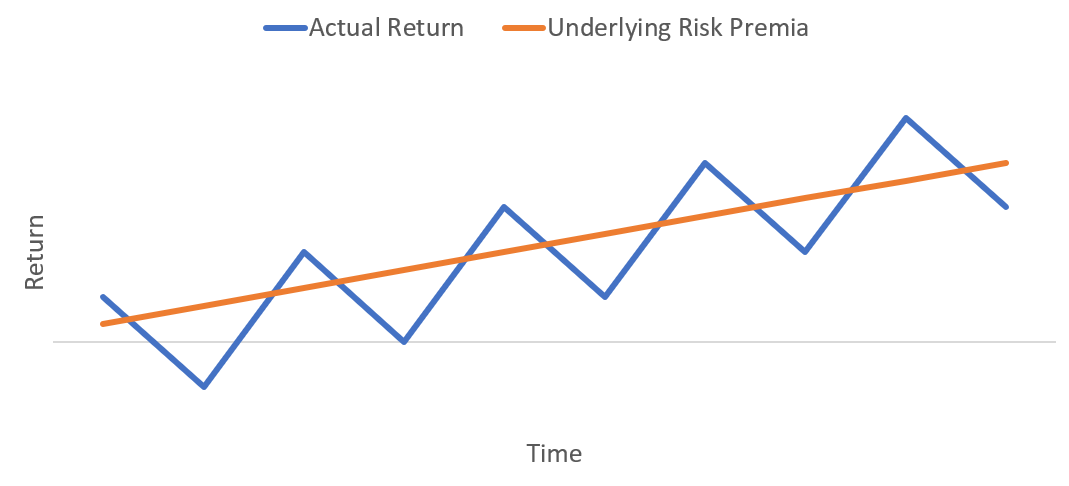

It helps to return to the basics of investment theory, which I discussed in my previous newsletter. Recall that your expected returns should look something like the following, with the blue line being your realized month-to-month returns, and the orange being the underlying "risk premia" - or "fair value" - that you are accumulating over time.

If you look at the past two weeks or so, we've most likely just experienced a very rapid cycle of this diagram, with assets moving temporarily above their fair value and now back below. The reason this is not particularly concerning is that it has no effect on your expected return over time, so long as you simply wait. By focusing primarily on long-term returns, you also minimize the many pitfalls of short-term timing and active management.

Now, Hedgewise still applies various kinds of risk management, but it is all with this long-term focus. For example, balancing exposures across many different assets, like stocks and bonds, tends to minimize the impact of a crash in any single one. But in the span of a few days or weeks when investors are panicking, it is possible they will all move down together. Likewise, there are certain extreme risk environments, like recessions and hyperinflation, that can sometimes be detected beforehand. But short-term market swings most often have very little to do with the economy at all.

With this perspective, the Hedgewise frameworks have continued to be quite effective. For example, since the beginning of 2018, the Hedgewise Risk Parity framework has lost significantly less than comparable major mutual funds. This continues a clear trend of outperformance ever since Hedgewise was launched. Last year, the Hedgewise Risk Parity and Momentum products both significantly outperformed the S&P 500 at the Max risk level, yet neither has lost significantly more than the S&P 500 so far this year.

Periods like these past two weeks will always be uncomfortable, but short-term losses are very different than long-term risk. To further make this case, let's take a deeper look at recent performance trends and how they stack up against history.

2018 Year-to-Date Performance: Unavoidable Losses, But Better Than the Competition

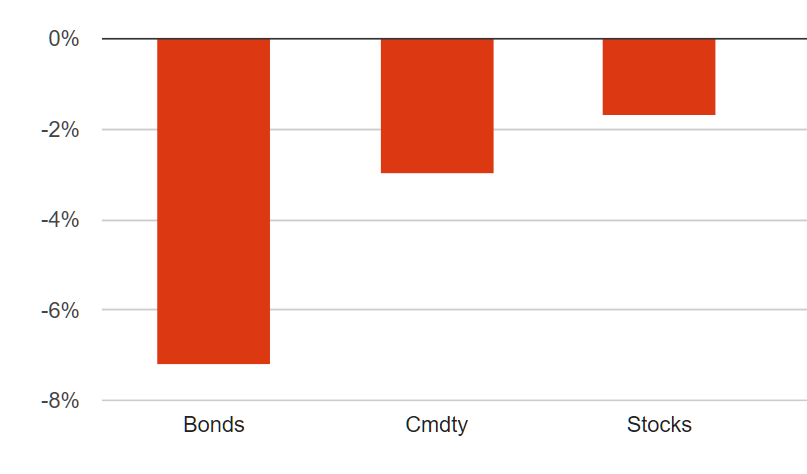

While most of the news is focused on stock returns since the peak on January 26th, equities were up almost 8% before they gave it all back. Trying to make sense of this fast of a reversal doesn't serve much purpose. The more interesting story is how various asset classes have performed year-to-date overall:

2018 Year-to-Date Performance By Asset Class

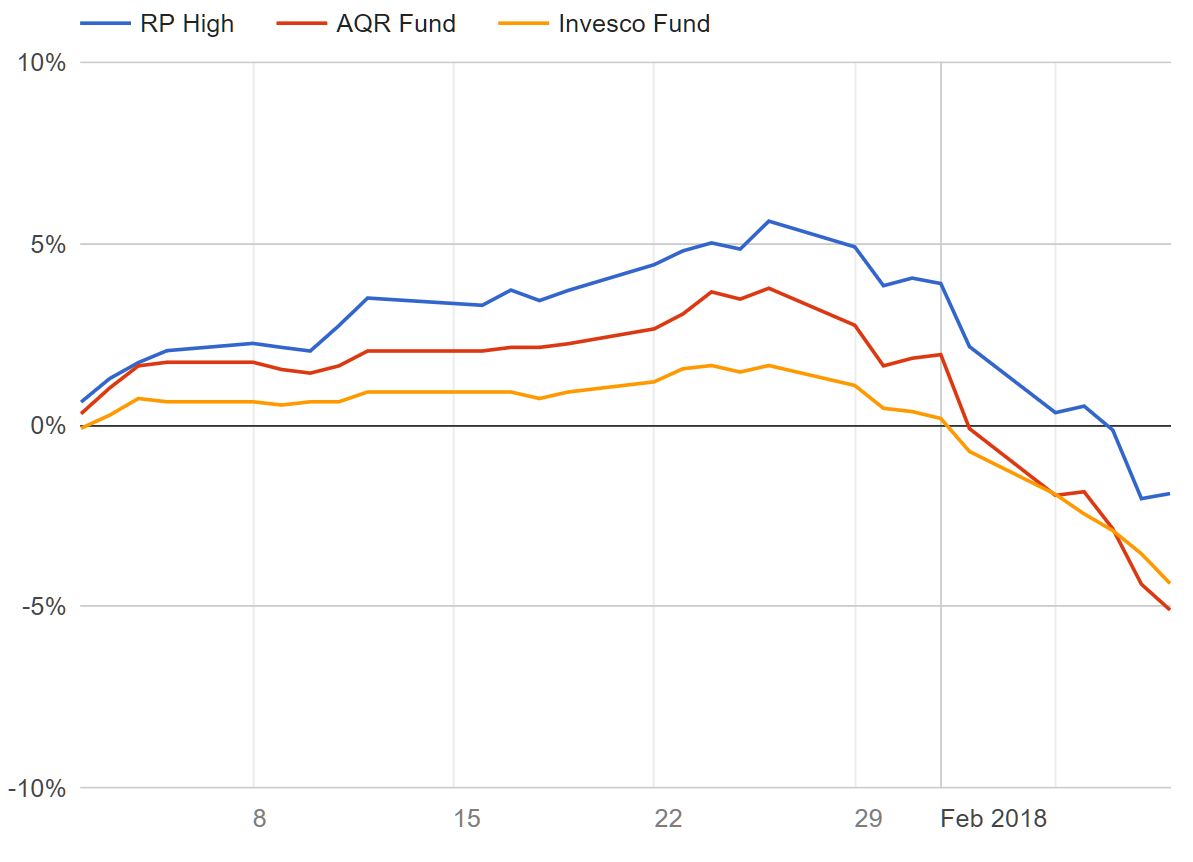

The bond market has actually been in a more significant correction than equities, as long-term yields have jumped about 0.7% since last September and 0.5% in the past two months alone. This makes some sense, given the Fed has started to more rapidly raise rates and reverse the "Quantitative Easing" program, and Hedgewise risk indicators have been frequently spiking as a result, including last month. The effectiveness of this dynamic risk management can be most easily seen by comparing the performance of the major Risk Parity mutual funds.

Performance of Hedgewise RP High vs Major Risk Parity Mutual Funds, 2018 Year-to-Date

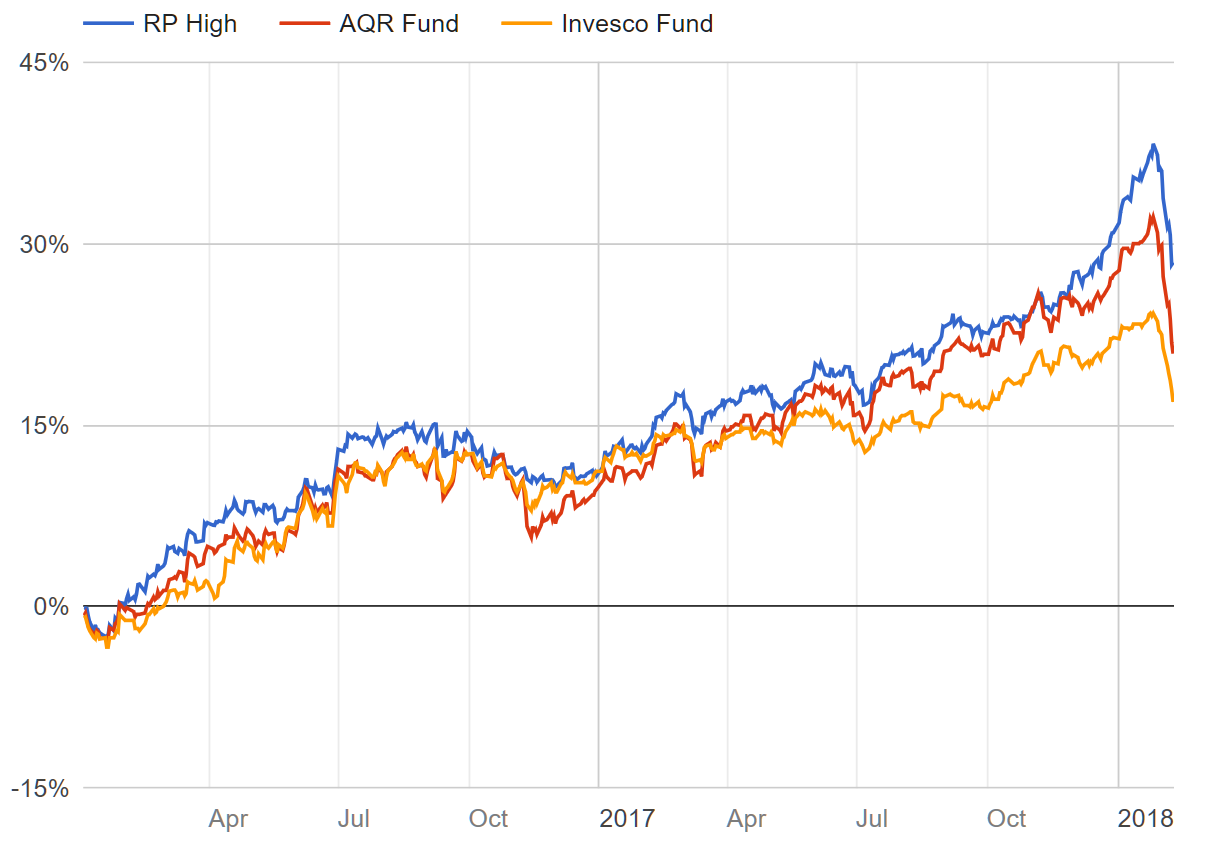

The graph continues to demonstrate a high correlation between the various risk parity products, since they are all investing in the same broad asset classes. The main difference is in how risk is balanced, and Hedgewise has consistently achieved a superior level of performance in the short and long-term, as demonstrated by its comparative performance back through the beginning of 2017.

Performance of Hedgewise RP High vs Major Risk Parity Mutual Funds, 2017 to Current

While the relative performance is excellent, why hasn't any Risk Parity framework been able to better hedge this equity correction? If you glance back at the year-to-date performance across asset classes, you'll notice that bonds, commodities, and stocks have all incurred losses simultaneously. In such an environment, there's really no way to avoid a loss unless you engage in very short-term timing (quick reminder: all active managers do some form of this, and over 90% of them underperform the S&P 500).

This kind of cross-asset correlation is somewhat exceptional, especially during a 10% equity correction, though not entirely unprecedented. Since 1970, there's been exactly four other scenarios where equities have lost 8% or more while safe havens like gold and bonds also suffered losses.

| Date | Event |

|---|---|

| Jul 1974 | Beginning of Stagflation |

| Dec 1980 | End of Stagflation; Interest rates peak near 20% |

| Oct 2008 | Beginning of Great Recession |

| Mar 2009 | Great Recession Market Bottom |

While these are some pretty scary events, the good news is that Hedgewise frameworks still did fine in all of these scenarios because safe havens eventually kicked in. Let's take a deeper look at how it unfolded.

When Safe Havens Fail: Why It Happens and What It Means

There are only two reasons that investors sell stocks, bonds, and commodities at the same time: either they are in full panic, or they are really confused about inflation. The Great Recession was a great example of 'sell everything' when Lehman went bankrupt. People just moved to cash in a mix of confusion and a need for liquidity. Gold was the logical hedge against a failing financial system, and it went on to rally by 30% by February 2009, but it often won't hold up at the outset.

Stagflation is the other culprit, since it means poor economic growth due to runaway inflation. Both stocks and bonds will lose money by definition (since higher inflation means higher interest rates). While real assets like commodities should do well since the dollar is losing its value, there's often an initial fear that the Fed will pre-emptively raise rates to fight inflation even if it will result in a recession. Ironically, a recession would then mean lower interest rates, so then bonds would actually rally, but you can see how everyone basically gets scared and confused!

In each of these scenarios, equities, bonds, and gold all fell together for a couple of weeks. To see how it eventually played out, though, I looked at the full one year return for each asset class following each event.

One Year Return by Asset Class After Initial Event

| Date | Stocks | Gold | Bonds | Jul 1974 | 15.2% | 16.4% | 5.6% | Dec 1980 | -2.8% | -36.6% | 11.6% | Oct 2008 | -9.2% | 14.1% | 7.7% | Mar 2009 | 62.3% | 18.8% | -2.7% |

|---|

What's really neat is that you can see all of the different possibilities unfold. While these were all pretty awful economic times, at least one of the asset classes eventually rallied. It's the laws of economics at work.

It's also helpful to look at how the Hedgewise models did over this same one year period after each initial event.

One Year Return by Hedgewise Model After Initial Event

| Date | RP Max | Momentum Max | Jul 1974 | 9.8% | 14.3% | Dec 1980 | -4% | 41.5% | Oct 2008 | 20.4% | 6.7% | Mar 2009 | 22.1% | 38.2% |

|---|

The big idea is that markets work themselves out over time, and that is eventually captured in the Hedgewise frameworks. You can still wind up with some bad years, and performance won't always bounce right back. But the odds are always on your side, perhaps even more so right after the scariest kind of market behavior.

Wrapping Up

While hopefully it's clear that there's no need to panic, whether losses have already bottomed or not, these past couple of weeks are still a wonderful opportunity to reflect on your own goals and risk tolerance. Investing presents a natural conflict between logic and fear. Rationally, targeting a higher long-term return seems like the right choice for many clients, despite the warning that a 20-30% loss is basically inevitable at least once a decade (at the higher risk levels). Yet it can feel quite different in the past couple of weeks when you see 10% disappear, and that's not even a particularly severe event!

On the other hand, the RP Max and Momentum Max product returned about 27% and 31%, respectively, in 2017 alone. Even if losses continue and this is the year of a 30% drawdown, you'd only be slightly worse off than if you had held cash the past year. It all depends on your perspective. Whether next month or next year, the drawdown will eventually come. If you remain patient and calm, it will also almost certainly pass. Either way, this most recent experience should help prepare and inform you.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.