Summary

- With tax season just past, it is a good time to study how Hedgewise helped to keep clients' tax bills down in 2014

- Our average client was able to defer thousands of extra tax dollars compared to an unmanaged account

- Since some assets are usually going down while others go up, the Hedgewise strategy is particularly suited to tax harvesting

- For clients with retirement accounts, Hedgewise further protected gains by intelligently allocating assets according to their tax efficiency

2014 Tax Savings for a Real Client

To give you a sense of how our tax strategy works, we selected a real client example that began an account in July 2014. This account was selected because it was one of our earliest clients which had approximately an equal proportion of assets in retirement and non-retirement portfolios. Here's how the account performed through the end of the year.

Client 2014 Tax Summary

| % | $ in a $100k account | Est. Tax Deferrals | |

|---|---|---|---|

| Total Performance | -1.0% | -$1,000 | $1,715 |

| Net Realized Losses | -6.2% | -$6,200 | $1,550 |

| Tax-sheltered Gains | 1.1% | $1,100 | $165 |

While the client did experience a small loss over this time period, their tax deferrals were significantly higher. In effect, a $100,000 portfolio was able to defer over $1,500 in taxes even though its actual loss was only $1,000.

What exactly does this mean? Though you will always have to pay taxes at some point, you can 'defer' them as long as possible through a technique called 'tax harvesting'. This means that you try to avoid paying taxes on your gains while immediately 'realizing' any of your losses. In effect, this pushes your tax liability further into the future, such that you can generate additional returns on that capital in the meantime.

Even better, any realized gains that happen within a retirement account are sheltered. In an ideal world, you could maximize your tax savings by keeping all of your realized gains in your retirement accounts and all of your realized losses in your non-retirement accounts.

Hedgewise automatically 'optimizes' every client account according to these principles, and it went almost exactly according to plan in 2014. Here's how.

Tax Harvesting with the Hedgewise Strategy

While tax harvesting is possible in any portfolio, it only works when you have losses to 'harvest'. This means it will often not be possible if you hold only a single ETF or mutual fund, and it may be less effective if your holdings are concentrated in a single asset class.

However, the Hedgewise strategy is particularly suited to reap the benefits of tax harvesting since it is constantly diversifying your portfolio across many different asset classes. For example, in 2014, the client discussed above had the following returns.

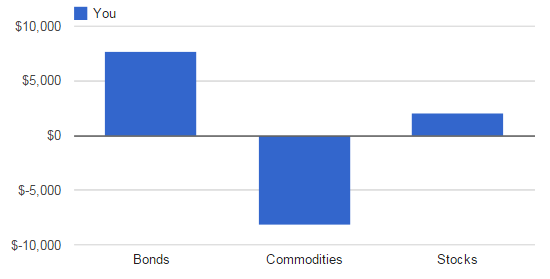

Client's Actual 2014 Returns By Asset Class

Hedgewise was able to continuously realize losses as commodities fell in value, while protecting its gains in bonds and stocks. Thus, the client was basically able to realize this entire loss in commodities, even though they had only a small overall loss in their account.

Moving forward, the natural diversification present in the Hedgewise portfolio will continue to provide such opportunities.

Tax Optimizing Your Retirement Accounts

In addition to tax harvesting, Hedgewise intelligently allocates assets between your non-retirement and retirement accounts, if you have any. By placing the assets with the highest expected tax impact in tax-sheltered accounts, we can even further increase your annual tax savings.

Hedgewise estimates each asset's expected tax impact based on a combination of your personal tax bracket, the underlying attributes of the asset, and the asset's expected annual return. For example, Treasury Bonds pay out monthly coupons that are taxable immediately, so it is usually beneficial to hold these in your retirement accounts. If our logic is working correctly, you'd see more realized gains in your retirement account, where they are tax-sheltered, and more realized losses in your non-retirement account, where they can be harvested.

Last year, this is how it turned out for our sample client.

| Realized Gains | Realized Losses | Total | |

|---|---|---|---|

| Retirement Account | $1,150 | -$50 | $1,100 |

| Non-Retirement Account | $500 | -$6,700 | -$6,200 |

In this case, it worked just as expected. The client experienced most of their realized losses in their taxable account, and most of their realized gains in their retirement account. This kind of intelligent optimization is quite unique, as most investment advisors simply manage retirement and non-retirement accounts separately. Hedgewise, however, manages multiple accounts under a single Target while taking into account your broader tax situation.

While the primary focus at Hedgewise will always remain on our underlying investment strategy, we also take every opportunity to further reduce costs and taxes for our clients. In 2014, we are happy to report this worked exactly as planned.

Key Takeaways

- Last year, Hedgewise used tax harvesting and optimization to help defer thousands of tax dollars for the average client

- Losses are continuously harvested while gains are protected, allowing you to push tax payments into the future and invest more today

- If you have both a retirement and a non-retirement account with Hedgewise, your investments are intelligently optimized to increase your tax savings even further

Hedgewise is not a tax adviser and assumes no responsibility to you for the tax consequences of any transaction. There is no guarantee that efforts to minimize taxes or to harvest losses in your account are successful. Hedgewise does not consider any of a client's personal accounts besides those which are directly under its management. This may create a conflict for tax purposes. You should confer with your personal tax adviser about all of your trading activities. Tax harvesting does not reduce your taxes, but rather shifts the tax savings to an earlier year. The primary benefit is the gain you may be able to make on that tax savings by investing it now instead of at a later date.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.