Summary

- In 2016, every Hedgewise product exceeded the performance of comparable benchmarks while incurring significantly lower risk of loss. Client portfolios achieved an average return of over 12%.

- The Hedgewise flagship product, Risk Parity, consistently outperformed competitive funds by 2% to 4% due to its superior risk management, lower costs, and tax efficiency. The portfolio remained stable throughout significant geopolitical events, such as the Brexit and the US election, continuing to prove its resilience in any economic environment.

- Hedgewise also launched two new products this year, Momentum and Long-Short Oil, as part of its broader vision to better fulfill any client goal. These products help risk-seeking clients achieve higher expected returns while maintaining the benefits of risk management, and initial results have been excellent.

Overview of 2016: Better Performance, Less Risk, More Innovation

2016 was a fantastic year for Hedgewise, which delivered on its core promise to clients: better returns with less risk of loss, whatever your goals. Here's a summary of how Hedgewise products performed last year compared to the S&P 500.

| Product | 2016 Performance | 2016 Max Loss |

|---|---|---|

| Risk Parity+ | 12.2% | -5.4% |

| Momentum | 24.0% | -6.4% |

| Long-Short Oil | 86.7% | -13.3% |

| S&P 500 | 11.7% | -9.1% |

These numbers tell the story quite well. For any given level of risk - with risk defined as the maximum amount you might lose - Hedgewise offers products that perform better than traditional alternatives.

Risk Parity is ideal for minimizing drawdowns while achieving equity-like returns. It frees clients from having to worry about the future by hedging for any economic scenario. This year, performance remained steady despite various pullbacks in both the stock and bond market, providing many great examples of the theory working in practice. Hedgewise also outperformed comparable Risk Parity mutual funds throughout the year, further differentiating its risk management techniques.

However, Risk Parity still has an upper limit on risk based on its need for leverage, which has natural caps for a variety of reasons. For clients with a greater tolerance for occasional large losses and a long enough time horizon, it often makes sense to prioritize higher potential returns over minimizing potential losses. To better cater to this need, I created the Momentum and Long-Short Oil Products.

The Momentum framework still takes advantage of the Hedgewise risk monitoring system, but concentrates exposure rather than disperses it. This makes it quite likely that clients may experience losses similar to equity markets, but with the potential for far greater returns. Initial results this year were consistent with this vision, as the Momentum strategy returned 24% overall, along with a higher corresponding level of volatility.

Long-Short Oil is the first Hedgewise "alpha" strategy, which means it has very little correlation to broader markets and is more speculative in nature. If executed well, such strategies are extremely valuable additions to a portfolio because they provide a completely independent return stream and another effective means of diversification. I am planning on developing a number of these strategies and helping clients layer them together to construct even higher performing portfolios.

Overall, 2016 represented another great step forward. Hedgewise now offers multiple risk-managed products, all of which outperformed. Not only that, Hedgewise helps clients combine these products together to create a portfolio which is even greater than the sum of its parts. As time goes on, I believe the benefits of this approach will only become more and more obvious.

Risk Parity Weathers Every Shock, From Stocks to Interest Rates

In theory, a Risk Parity portfolio should create more stable, positive returns over time because it is constantly hedged for any kind of economic scenario. A number of events during 2016 helped to demonstrate that this is working just as it should:

| Event | S&P 500 | Risk Parity+ |

|---|---|---|

| Jan-Feb Stock Correction | -9.08% | 1.37% |

| Brexit | -5.57% | -1.08% |

| Pre-Election Jitters | -3.3% | -1.37% |

For most investors to avoid the risk of these events, they must rely on overly conservative portfolios with limited upside. However, the Hedgewise Risk Parity framework achieved this stability while still outperforming the S&P 500 for the year.

This is extremely powerful both financially and psychologically. Prior to the Brexit and the US election, I had numerous clients asking whether they should consider lowering their risk levels or liquidating altogether. My advice was to remain steady, as the strategy was already built to handle such events. However, investors in traditional portfolios had no such security, and were often compelled to jump in and out of the market or to remain in cash. This is a significant hidden cost to most investors. Risk Parity eliminates the need for this kind of timing concern and thus protects investors without sacrificing long-term returns.

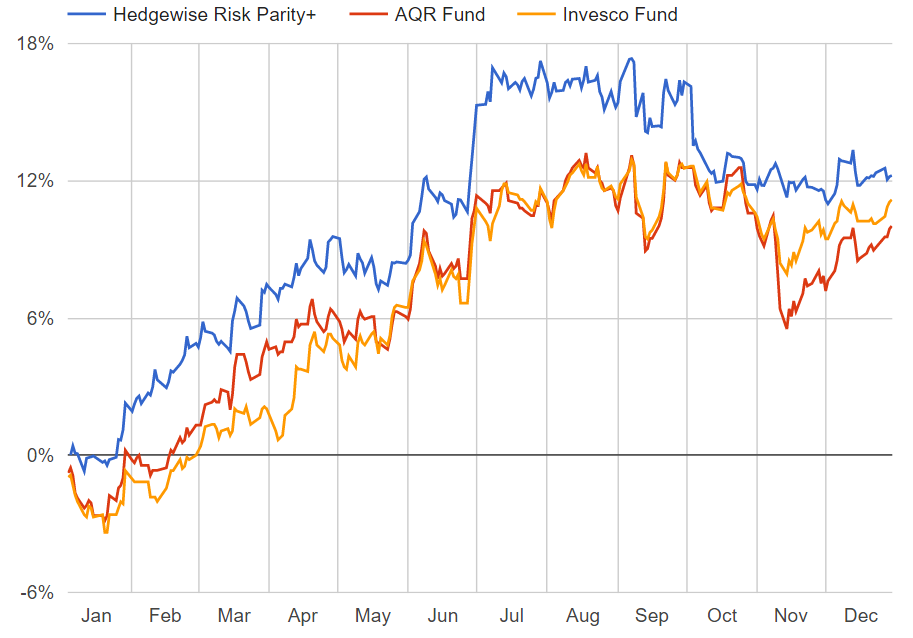

While Risk Parity is an excellent general framework, it can be run in many different ways. In 2016, Hedgewise proved that its approach to managing risk and balancing assets is superior to that of other providers.

AQR and Invesco run two of the largest Risk Parity mutual funds. Last year, Hedgewise maintained a high overall correlation to these funds while consistently outperforming both. Hedgewise also accomplished this while charging half the fees and incurring a significantly lower tax burden for every client.

Hedgewise 2016 Risk Parity+ Performance vs. Competitors

For clients who remain nervous about the future, especially in the stock market, Risk Parity has consistently proven to be a safer way to grow your money.

New Momentum Framework Drives Higher Potential Returns

While Risk Parity is an excellent product, it is naturally somewhat conservative even at the highest risk target. This is because it is hedged across many different assets, which drives stability above all. For younger or more speculative clients, though, stability is often not the primary goal. They might gladly accept a few years of large losses in exchange for a higher overall return. The new Hedgewise Momentum framework helps to address this need.

Generally, "Momentum" refers to the use of various timing signals to reduce the risk of significant drawdown events on your portfolio. Unlike Risk Parity, this means you concentrate risk in certain markets most of the time, rather than diversify. For example, you might stay 100% in equities unless you hit some sort of downside trigger, and 100% bonds otherwise.

However, similar to Risk Parity, the success of any Momentum strategy depends entirely on the quality of its risk management system. Whenever a timing signal fails, you run the risk of incurring significant losses and/or missing potential gains. Since Hedgewise already has deep risk management expertise, though, it made sense to translate that into a timing framework.

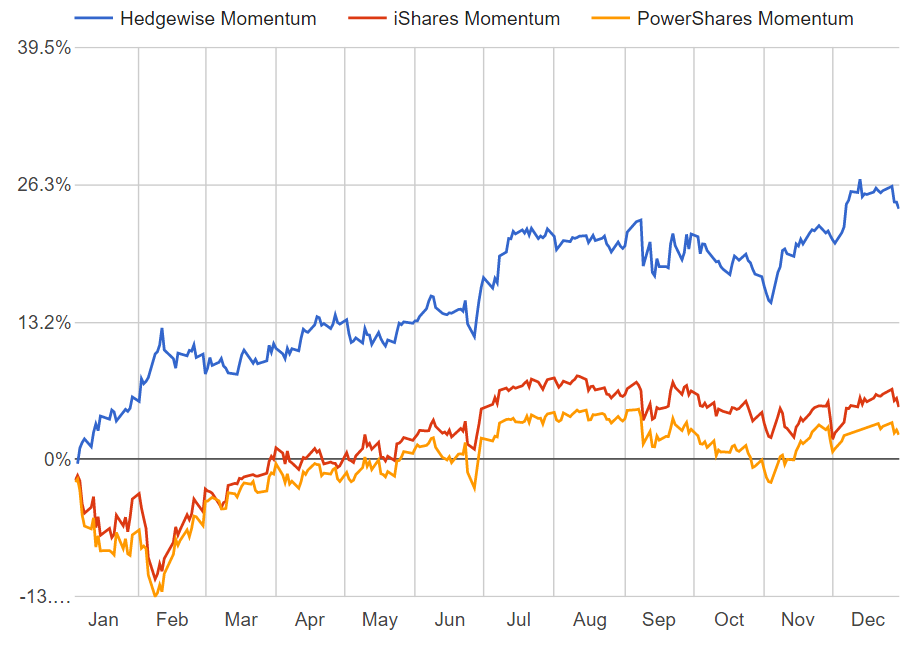

While I am planning on publishing additional literature on this strategy later this year, the early results have been excellent. Here's a look at the model's performance for 2016 compared to a couple of the largest competitive Momentum ETFs on the market. You can quickly see how much performance is driven by getting the signals right - or wrong.

Hedgewise 2016 Momentum Performance vs. Competitors

While returns this year were very high, they come with additional risk. You maintain some protection from drawdowns, but it is not nearly as robust or layered as Risk Parity. As such, it makes sense to view this as a more "equity-like" return stream, including the possibility of a year like 2008. However, in exchange for that possibility, you gain the potential for far higher returns - like the 24% achieved in 2016.

This is an especially attractive proposition for investors who have most of their money in equities already. Since they are already assuming the risk of a year like 2008, why not utilize risk management to potentially boost returns further?

When discussing this product with clients, there is often confusion as to how to choose between Momentum and Risk Parity. Luckily you don't have to. Just like diversifying across assets makes a portfolio more robust, so does diversifying across risk management frameworks. This kind of quantitatively-driven portfolio construction is unlike anything you else you can find on the market.

Looking Forward to 2017

While lots of research is continuing behind the scenes, Hedgewise has already become a very powerful investing platform. Each individual Hedgewise product outperformed the competition as well as the S&P 500 last year. Whether your goal is conservative or aggressive, Hedgewise can customize a portfolio to exactly suit your needs. By combining different products together, clients have access to an even more robust portfolio. All of this can be done without any additional fee and in any kind of account - IRAs and even 401ks.

Despite this progress, there is still so much more potential. Unlike ETFs and mutual funds, Hedgewise is constantly continuing its research. Soon, there will be a number of alpha streams to choose from and advice on how to optimally layer them into your portfolio. More improvements will be made to the underlying risk system behind Risk Parity and Momentum. Hedgewise already offers a best-in-class product, but there is always the potential to make it even better.

I'm excited to continue to share the results, and 2017 is already off to a great start.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.