Summary

- Investors in our Risk Parity fund have had their patience rewarded this year, gaining anywhere from 3 to 6% (depending on your risk level) while equities have tumbled.

- This highlights the benefit of keeping a properly risk-balanced portfolio, which we expect will continue to shine within the current market environment.

- In all likelihood, we are nearing the end of the current bull market, with many cracks in the economy already beginning to show.

- We discuss why this makes risk parity an even more compelling strategy over the next few years.

Patience Is Rewarded In 2016

In our year-end newsletter, we highlighted that risk parity tends to be countercyclical to equity bull markets. The strategy naturally underperforms when stocks are the highest performing asset class, and vice versa. However, since no bull market lasts forever, risk parity still outperforms over the long-run. You simply need to live through one bear market to see why.

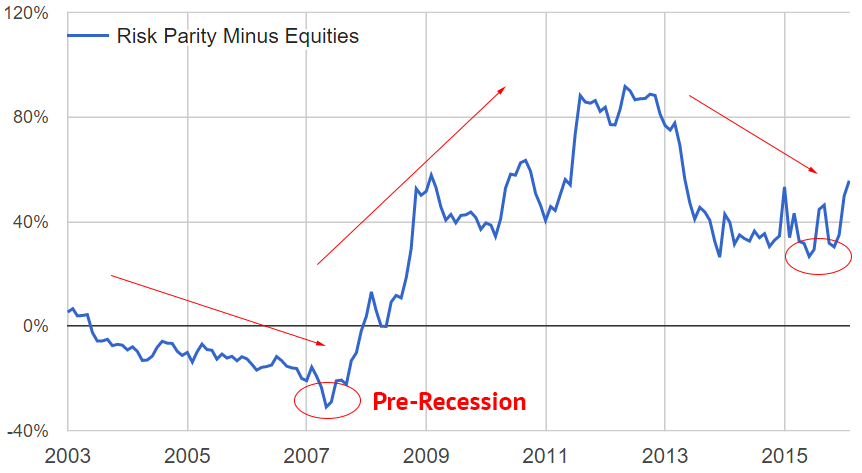

It is easy to see these cycles by examining the relative performance of a model risk parity portfolio to the S&P 500 over time.

Model Risk Parity Performance Minus S&P Performance Since 2003

As highlighted in the graph, the risk parity portfolio tends to look the worst right at the tail end of a business cycle, when stocks are near their peak. As soon as a significant equity correction occurs, though, the performance quickly corrects and tends to remain net positive even through the next down cycle.

While this can be trying during periods like last year, patience has always been rewarded, and it has been again so far in 2016. As the likelihood that our current bull market is coming to an end increases, so does the likelihood that the risk parity approach continues to shine.

Why Is Risk Parity Outperforming?

Last year, global weakness caused an epic crash in the commodity markets, yet the Fed proceeded to raise U.S. interest rates, the Dollar rallied, and the stock market basically shrugged. In our December newsletter, we noted:

"We've had a combination of a relatively strong economy, low inflation, and plummeting global prices for raw materials. Put simply, this situation is not particularly normal. In fact, it has only occurred a handful of times over the past 30 years, almost all of which involved a major geopolitical event, such as the beginning and subsequent end of an oil embargo. Today, we are witnessing a similar economic situation despite the absence of any such event, and there are many reasons to believe it cannot last."

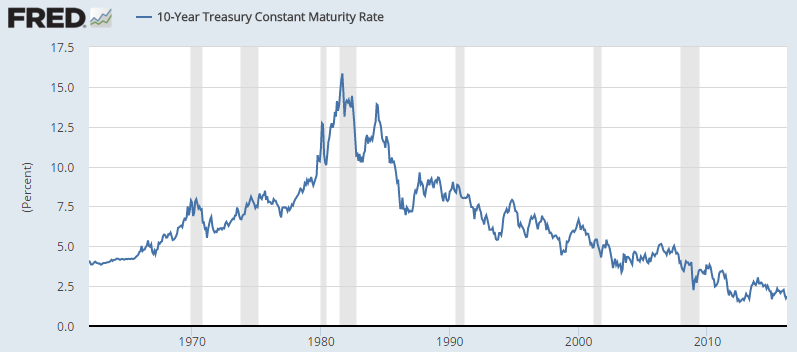

Fast forward to today, and it has become far more clear that the U.S. cannot simply shrug off continued economic weakness around the world. The strong dollar and struggling global economy has left U.S. exports at a five-and-a-half year low, the Dollar has pulled back significantly since the beginning of the year, and interest rates on 10-year Treasuries have nearly returned to their lowest levels ever.

10-Year Treasury Interest Rates since 1962

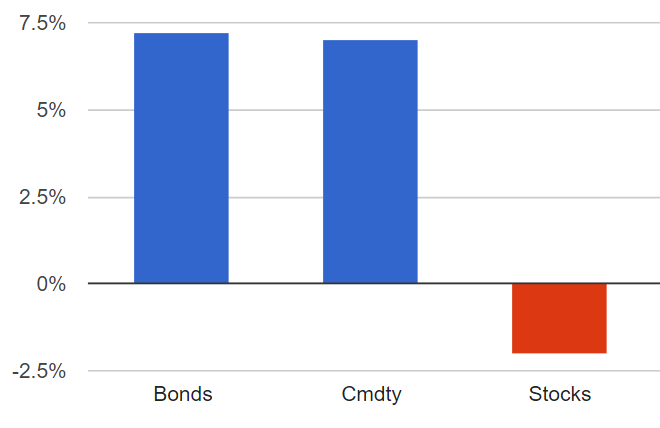

Against this backdrop, both bonds and commodities have had significant rallies this year, putting markets back into more sensible balance, and driving positive performance in the risk parity portfolio.

Year-to-date performance of Major Asset Classes

Why Does Risk Parity Make Sense Moving Forward?

Our performance reversal this year highlights the fact that although markets can certainly do strange things, they tend to return to balance in a relatively short timeframe. As soon as balance prevails, the risk parity portfolio generally yields positive returns regardless of the economic environment. In recessions, bonds and gold tend to offset weakness in stocks. In expansions, stocks and commodities tend to offset weakness in bonds. During periods of high inflation, real assets like oil hedge the risk of a plummeting currency.

By retaining this constant balance, investors are freed from trying to predict the future. Few might have anticipated such a huge bond rally this year back in December, when the Fed was poised to raise interest rates four times in 2016, but it happened nonetheless. While skeptics of risk parity often point to the certainty of rising interest rates, the first few months of this year have shown that it is far from inevitable.

In fact, various countries around the world have now entered into a negative interest rate environment, a scenario which many economists thought could not possibly unfold. Yet it has, and it means that current U.S. interest rates still have room to drop even further if we face renewed economic weakness.

While the U.S. may not be facing an imminent recession, it is hard to envision a scenario where stocks have much upside. Unemployment is already below 5%, and the current bull market is steadily approaching the second longest in history. While this is a scary prospect for most investors, it is just such situations that show the incredible power of the risk parity approach. As the first few months of 2016 have already shown, weakness in the stock market can still result in gains to your portfolio. It doesn't require short-term market timing, nor does it force you to concentrate your holdings into a single asset class.

We are confident that the wins of this year will be one of many in the near future, and extremely grateful to our clients for maintaining perspective and staying patient. Risk parity remains an excellent investment choice even among volatile markets, and we look forward to continuing to prove it to you.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.