By using derivative contracts, such as options and futures, you can generate leverage in your portfolio at an interest rate only slightly higher than US Treasury Bills. As of 2016, this means you can essentially give yourself a loan with an underlying interest of about 0.5%! Since most retail investors do not have portfolios large enough to justify the use of futures, this article will focus on how to use options contracts to generate leverage.

Derivative contracts are always based on some underlying security, like a stock. Because of this, it is easy to take the opposite side of a contract and create "arbitrage", which is a form of guaranteed return. For example, with an options contract, selling a call and buying put at the same strike price and termination date is equivalent to shorting 100 shares of the underlying stock. If you buy 100 shares of that stock at the same time, you no longer have any risk of loss as the positions completely offset.

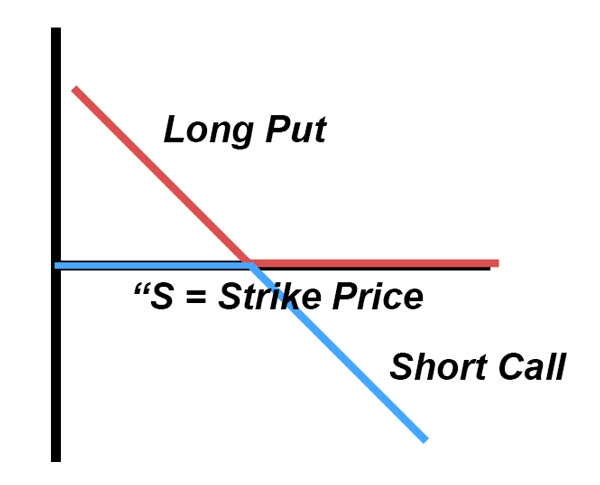

To illustrate this, here is the payoff diagram at expiration of a long put and short call at the same strike price. If you also were also long 100 shares of the underlying stock, the positions would entirely offset.

Option Contract Payoff Diagram

For example, let's say you bought 100 shares of SPY at $200 per share, for an initial outlay of $20,000, and went long a put and short a call at a strike price of $200 at the same time. Assume the options expire in 3 months.

If at the end of 3 months, the price of SPY goes up to $210, you make $10 on your stock shares, but you lose $10 on your call contract. Conversely, if the price goes down to $190, you lose $10 on your stock shares, but you make $10 on your long put. Thus, there is no risk of loss when you hold this combination of positions.

The arbitrage opportunity is determined when you initially purchase the contracts, as you will be paying a premium when you buy the put and receiving a premium when you sell the call. If you receive more for the call than you do for the put, that would be a guaranteed profit since there is no risk of future loss.

If put prices got too high, or call prices got too low, anyone in the marketplace could put together this combination and pocket the difference. They just need to have enough capital to purchase the underlying shares, and then wait until the options expire. Generally, the difference will settle out to be pretty close to the risk-free interest rate plus 0.3% to 0.5%. For example, if you had to put up $20,000 to buy this combination of positions for 3 months, and the risk-free rate was 0%, you'd expect payment of 0.3% to 0.5%, or $60 to 100. These forces are what help determine the relative pricing of put and call contracts in real-time, and there are enough players in the market to ensure that this interest rate never gets too high.

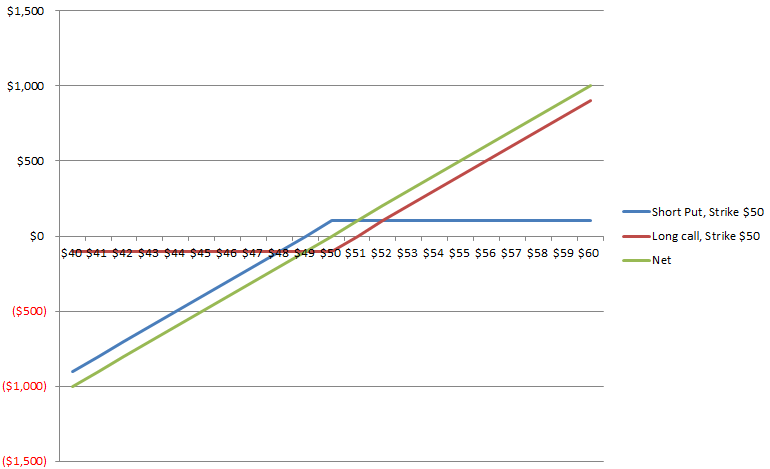

This arbitrage ensures that any combination of a long/short call and a short/long put, at the same strike price and expiration date, generally carries a similar interest rate. To take advantage of this situation to generate leverage in your portfolio, you can simply purchase that combination of options contracts. For example, instead of buying 100 shares of SPY, you'd go long a call and short a put on SPY at the same strike price and expiration date. This is known as a "synthetic long".

Option Contract Payoff Diagram - "Synthetic Long"

Note that the final payoff is equivalent to as if you owned 100 shares of the underlying. However, the amount of capital you needed to create this position is about 20% to 25% as much as if you had bought the shares outright. In other words, instead of buying 100 shares for $20,000, you were able to get the exposure for $4,000 to $5,000. You'd expect this position to perform exactly the same as if you had bought 100 shares, minus the cost of the interest rate discussed above.

It's easy to show real-life examples that this works quite well, since Hedgewise builds these kinds of contracts for its clients all the time. Here are a couple of examples using completely real market data.

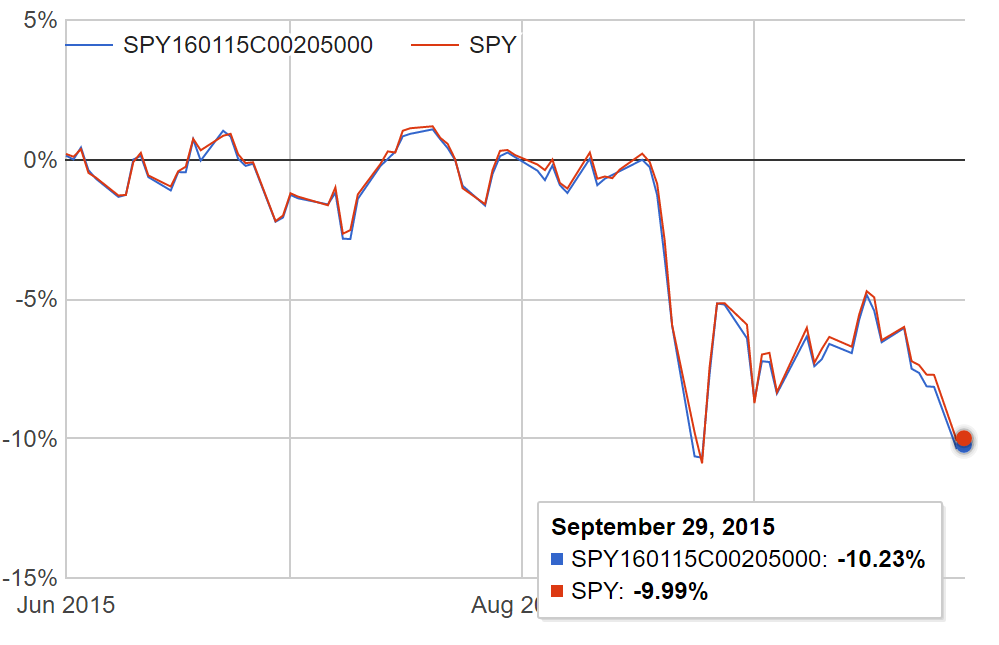

Example 1: SPY options, $205 strike, expiring January 15, 2016

This is the SPY synthetic long option with a termination date of January 15, 2016 and a strike price of $205. The options contracts were purchased at end-of-day prices on June 1, 2015, and liquidated at the end of September. The total performance difference over this four-month period was 0.26%, including all dividends. This translates to an annualized "interest rate" of about 0.8%.

The total capital required to create the options position was about $5,000, compared to about $20,000 that would have been needed to buy 100 shares. That means you generated leverage of approximately $15,000 in your portfolio.

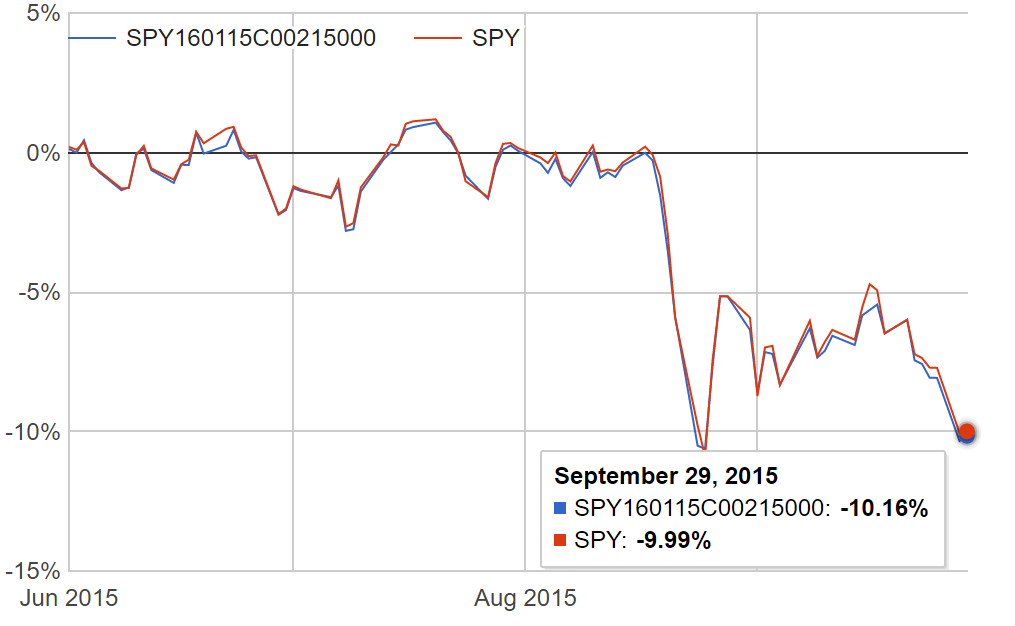

Example 1: SPY options, $215 strike, expiring January 15, 2016

This next example illustrates that the strike price of the option contracts does not matter. The premiums of the call and put contract automatically adjust to account for any difference between the strike price and the current spot price. The option gamma and vega offsets since you own both sides of the contract.

The total performance difference for this contract was 0.183%, or an annualized interest rate of 0.55%. Note that the exact interest rate can be calculated based on the option premiums at the time of purchase and thus will vary slightly depending on your execution prices.

Caveats

You should only consider implementing this kind of strategy if you are deeply familiar with how options contracts work and the associated risks. It is recommended that you calculate the implied interest rate on every combination of contracts before executing any trade. These positions require that margin be set aside in your account, and there is the possibility of having a margin call if you experience a significant loss. Written options contracts may also be exercised early, which would require you to immediately re-adjust your portfolio and could create additional risk.

Footnotes

1 Performance figures use end-of-day price data and do not account for spreads or commissions. Hedgewise provides no guarantee as to the accuracy of the data. The performance is not based on any real portfolio and does not constitute a recommendation to any client.

2 The use of derivatives exposes your portfolio to potentially increased cost due to interest, spreads, and lost dividends. These derivatives also require that some cash be set aside in your account as margin for each contract, known as a 'margin requirement'. Large and sudden losses may cause the brokerage where your assets are held to forcibly liquidate your positions to meet the margin requirement. American-style written naked put options also have the risk of early exercise, in which you would be required to purchase the underlying asset at the strike price of the option. Both of these circumstances would require an immediate account rebalancing and would result in additional risk and cost.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.