Summary

- Hedgewise did not invent the "risk parity" strategy. However, we have innovated in a number of ways to make it smarter, cheaper, and more accessible for individual investors.

- The competitive mutual funds in this space have an annual expense fee as high as 2% and tend to be relatively tax inefficient. Many are also closed to new investors.

- While our competitors play a more "active" role in management, our theory is that a more efficient and systematic approach will still capture most of the benefits while significantly lowering costs with lower fees and tax-loss harvesting.

- Moving forward, we will be benchmarking our performance to a leading fund in the space. While results will inevitably be different for a number of reasons that we outline below, we will be transparent in showing you how the approaches compare over time.

Introduction: Our Approach to Risk Parity

As we've discussed in some of our earlier articles, risk parity is a fancy name for a fairly simple concept: a properly diversified portfolio will tend to achieve a better return with a lower risk of loss. Risk parity seeks to continually pinpoint this point of 'optimal diversification' with a framework that balances risk across different types of assets.

Our approach to the strategy has been to begin with these principles and avoid adding unnecessary cost or complexity. Just as Vanguard has already proven with its own passive indexes, we believe that an inexpensive and systematic approach to investing will often outperform more active efforts. However, up until this point, such an approach did not exist for the risk parity framework.

There are two primary reasons for this. First, the idea of 'optimal diversification' can become a bit unwieldy. Ideally, you could invest in every asset class available across the globe, but this presents a number of challenges. Global investing presents problems like currency exposures, and many types of commodities can only be traded via futures contracts, which often come with additional cost and complexity.

Second, much like the early days of mutual funds, investment managers often apply their own judgment to the theory, much like 'stock picking', but in this case, it has become 'asset class picking'. This kind of 'active' approach commands higher management fees with the pretext that it is adding value.

As a result, the competitive mutual funds in the space tend to be quite complex and pricey. Since the core concepts are so simple, though, our approach at Hedgewise is to run a version of the strategy that is entirely systematic (not 'active') and uses only highly liquid, US instruments. This enables us to offer it at lower cost, with greater tax efficiency, and customized to each client's target level of risk and return.

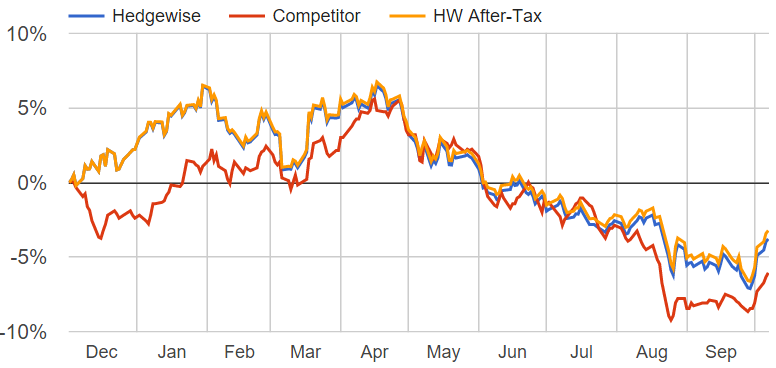

We discuss the implications of some of these trade-offs in greater detail below, but thus far we believe our relative performance speaks for itself. We will also be keeping this graph updated daily on our strategy overview page for full transparency moving forward.

Hedgewise Target 10% Performance versus Leading Competitor, Dec 2014 - October 2015

Systematic Risk Management

Every provider of this strategy must have a system to measure and balance risk across asset classes. While it is quite unlikely that any two frameworks will be exactly the same, they will inevitably be centered on similar concepts. Each asset class has fundamental attributes that give rise to the possibility of loss. In bonds, the current level of interest rates drives risk factors like duration and convexity. In stocks, macroeconomic factors play a large role. These fundamentals form a natural basis for estimating risk. Beyond these, historical and implied volatility provide additional guidance on how risk may be changing at a given point in time.

We provided some additional commentary on our approach to risk in this article, but the general idea is that any quality system will yield fairly similar estimates. Tweaks to one framework versus another may change performance slightly over time, but not drastically.

However, we strictly avoid using human judgment to adjust our risk estimates, which is really no different from active management. This is a key differentiator from our competitors, who regularly adjust up or down certain exposures based on their current opinion of the market. Our belief is that such active decision making tends to be very difficult over the long run, especially given the higher fees that come along with it.

Highly Liquid, US Only

In a completely ideal world, you would be able to diversify across every asset class imaginable: equities, fixed income, credit, real estate, and commodities across both developed and emerging economies. In theory, every independent return stream would better balance your return over time.

In practice, though, many types of investments come with undesirable baggage. If you invest in a foreign economy, you are then exposed to that currency, which you must hedge out using FX instruments. Creating these hedges comes with additional cost, and it may even be impossible with smaller portfolios.

Some asset classes, like credit, do not have highly liquid instruments available. You must use more exotic contracts like 'credit default swaps', which may need to be created with a single counterparty rather than over an exchange. This introduces additional default risk if that counterparty cannot fulfill its obligation for some reason, which was a huge problem during the crisis of 2008. In addition, any exotic contract will have little liquidity, which tends to increase the cost of purchase.

Finally, many exposures may not prove to be 'independent' return streams, which is a key part of diversification. For example, adding large-cap stocks and small-cap stocks to a portfolio which already owns the S&P 500 will have little diversifying affect: every exposure has the same underlying risk factors. Adding elements with such marginal impact will tend to increase costs without much benefit.

In our approach, we assume that the cost of foreign and/or illiquid exposures will often negate any positive impact. We also believe that you can get nearly the entire benefit of this strategy using only broad-based US indexes due to the increasingly connected global economy. For example, during the crisis in 2008, the stock markets of nearly every developed economy crashed while bond markets rallied. Whether you had a balanced portfolio of stocks and bonds in the US alone, or in every other country, the net result was about the same.

Avoid Tail Risk

On a related note, many exotic exposures have a difficult to quantify but significant underlying tail risk. That is, there is a very small probability of an extremely large loss. In credit default swaps, for example, one party receives a small but constant payment in exchange for guaranteeing the other party that some underlying investment will not default. If that investment does default, the first party is suddenly on the hook for a huge sum.

We strictly avoid these kinds of risks because it is so difficult to model them and to effectively diversify a portfolio against them. Any benefit they provide may be suddenly and unexpectedly wiped out in an instant.

Lower Fees, Tax Efficient, and Customizable

By structuring our portfolio in this way, a number of additional benefits become available. First, our fees and net costs are far lower than the competition. Second, we are able to lower any tax burden through the use of tax-loss harvesting and tax-efficient portfolio allocation. Finally, we allow each client to control their own desired level of risk and return and to change it at any time.

Wrapping Up

Risk parity is a very intelligent approach to long-term investing that should be available to anyone that wants it. Our first year of performance is comparable to best-in-class mutual funds, and while there will inevitably be some deviation between providers, we offer you full transparency into what is driving the difference. Over the long run, we are confident that our combination of a systematic approach, lower fees and taxes, and customizability will prove to be a superior option for savvy investors. We look forward to continuing to prove it to you.

Disclosure

This information does not constitute investment advice or an offer to invest or to provide management services and is subject to correction, completion and amendment without notice. Hedgewise makes no warranties and is not responsible for your use of this information or for any errors or inaccuracies resulting from your use. Hedgewise may recommend some of the investments mentioned in this article for use in its clients' portfolios. Past performance is no indicator or guarantee of future results. Investing involves risk, including the risk of loss. All performance data shown prior to the inception of each Hedgewise framework (Risk Parity in October 2014, Momentum in November 2016) is based on a hypothetical model and there is no guarantee that such performance could have been achieved in a live portfolio, which would have been affected by material factors including market liquidity, bid-ask spreads, intraday price fluctuations, instrument availability, and interest rates. Model performance data is based on publicly available index or asset price information and all dividend or coupon payments are included and assumed to be reinvested monthly. Hedgewise products have substantially different levels of volatility and exposure to separate risk factors, such as commodity prices and the use of leverage via derivatives, compared to traditional benchmarks like the S&P 500. Any comparisons to benchmarks are provided as a generic baseline for a long-term investment portfolio and do not suggest that Hedgewise products will exhibit similar characteristics. When live client data is shown, it includes all fees, commissions, and other expenses incurred during management. Only performance figures from the earliest live client accounts available or from a composite average of all client accounts are used. Other accounts managed by Hedgewise will have performed slightly differently than the numbers shown for a variety of reasons, though all accounts are managed according to the same underlying strategy model. Hedgewise relies on sophisticated algorithms which present technological risk, including data availability, system uptime and speed, coding errors, and reliance on third party vendors.